The World Health Organization recently declared that Covid-19 is no longer a global health emergency. While the pandemic threat has waned, there continues to be huge unmet need for affordable essential medicines to treat chronic diseases that kill 41 million people each year. Over the last two decades, Biocon has been at the forefront of providing cost-effective generics and biosimilars to address the therapeutic needs of a global patient pool.

Enabled by continued investments in building strong R&D capabilities and large-scale manufacturing facilities over the years, Biocon is positioned perfectly to be at the forefront of driving inclusive and equitable healthcare. The robust financial performance in FY23 is an outcome of our untiring efforts to enhance global healthcare through high-quality, affordable biopharmaceuticals.

The year gone by saw the completion of Biocon Biologics’ landmark acquisition of Viatris’ biosimilars business, which has contributed to the year’s growth. This strategic investment will accelerate our journey to global leadership, as a fully integrated biosimilars player.

A Strong Annual Performance

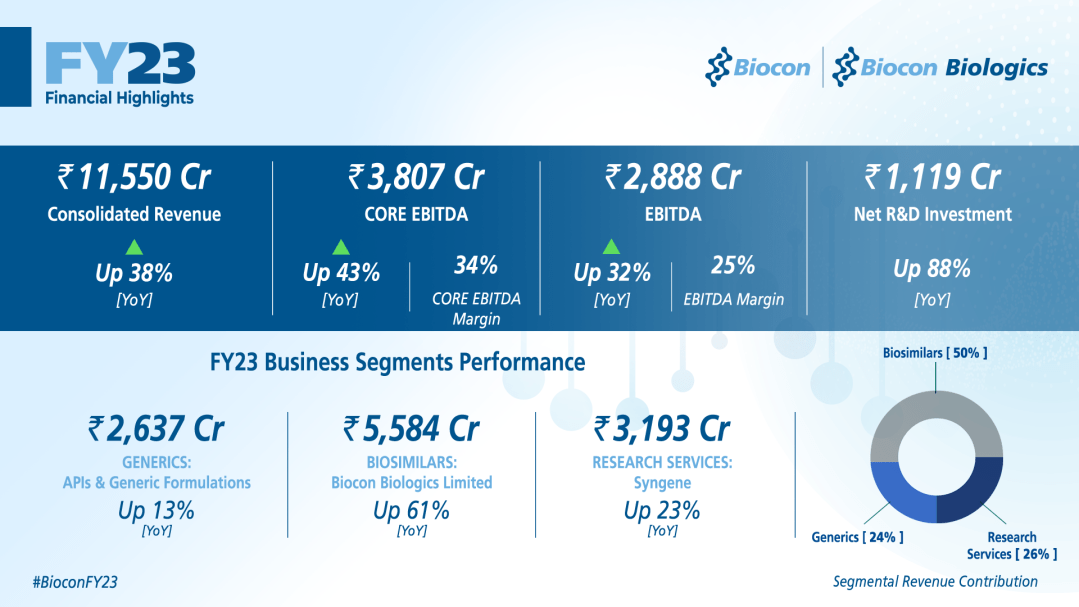

Biocon’s consolidated revenues grew 38% to Rs 11,550 crore for the full year, led by Biosimilars revenues increasing 61%, as well as Research Services and Generics revenues rising 23% and 13%, respectively.

For the year, revenues from the Biosimilars business grew robustly to Rs 5,584 crore (Rs 3,464 crore in FY22), contributing to ~50% of total consolidated revenues. The Research Services business grew to Rs 3,193 crore (Rs 2,604 crore in FY22), which accounts for ~26% of total consolidated revenues. The Generics segment reported revenues of Rs 2,637 crore (Rs 2,341 crore in FY22), accounting for ~24% of total consolidated revenues.

EBITDA grew 32% to Rs 2,888 crore (Rs 2,183 crore in FY22), with margins at 25%.

With three of our antibodies, Ustekinumab, Denosumab and Pertuzumab in the clinical phase, which represents a large part of the overall cost that goes into developing a molecule, R&D spends for the full year increased by 88% to Rs 1,119 crore (Rs 595 crore in FY22). The investments on R&D are core to our growth strategy as it enables us to bring more products into the market in both Generics and Biosimilars.

Adjusted for R&D expense, licensing income, forex movement, dilution gain in Bicara and mark-to-market movement on financial instruments, Core EBITDA for the year grew 43% to Rs 3,807 crore (Rs 2,669 crore in FY22), representing a margin of 34% (versus 32% in FY22).

Profit Before Tax and exceptional items stood at Rs 1,189 crores, up 9% year-on-year. The growth in PBT is not commensurate with growth in EBITDA due to additional depreciation, amortisation and interest charges, primarily related to the biosimilar business acquisition.

Consequently, Net Profit for the year before exceptional items stood at Rs 787 crore versus Rs 722 crore in FY22, up 9% year-on-year.

For the full year FY23, there were exceptional items amounting to Rs 324 crore, net of tax and minority interest, as compared to Rs 74 crore in the last fiscal. These include deal related expenses of the Viatris transaction and a MAT credit balance charge, as Biocon decided to adopt the new tax regime of 25%.

As a result, Net Profit for FY23 stood at Rs 463 crore.

Good Quarterly Financials

Total Revenue for the quarter was up 59% year-on-year to Rs 3,929 crore. The Biosimilars segment revenue more than doubled on the back of the acquisition of Viatris’ biosimilar business, with Q4 reflecting the first full quarter of consolidation.

Research Services grew 31% while Generics remained muted.

Core EBITDA grew by 56% to Rs 1,260 crore, representing continued healthy core operating margins of 35%.

R&D spends for Q4 stood at Rs 342 crore, an increase of Rs 152 crore as compared to the same period last fiscal.

EBITDA for the quarter was up 75% at Rs 1,152 crore versus Rs 659 crore in same period last year. EBITDA margin stood at 29% as compared to 27% in Q4FY22.

Depreciation, amortisation and interest increased by Rs 389 crore over last year. This is primarily related to the biosimilar business acquisition cost.

Consequently, Profit Before Tax and exceptional items stood at Rs 500 crore, up 30% year-on-year.

Net Profit for the quarter excluding exceptional items stood at Rs 335 crore versus Rs 262 crore in Q4 FY22, up 28% year-on-year.

Net Profit for the quarter rose 31% to Rs 313 crore from Rs 239 crore in the same period last year.

It was a transformative year for the Biocon group. All three business segments are at an inflection point and poised for significant growth in the years ahead.